Renovate or Relocate?

The 2026 DMV Economic Analysis: a data-driven framework for the biggest financial decision a homeowner faces.

Published June 2026 | Four Seasons Home Improvement | Serving the DMV Since 1976

Executive Summary

Every homeowner in the Washington, D.C. metro area eventually faces the same question: should I renovate the home I have, or sell it and buy something that better fits my needs? It feels like a personal decision — and it is — but it is also, fundamentally, an economic one, and it can be analyzed with real numbers drawn from the 2026 DMV housing market.

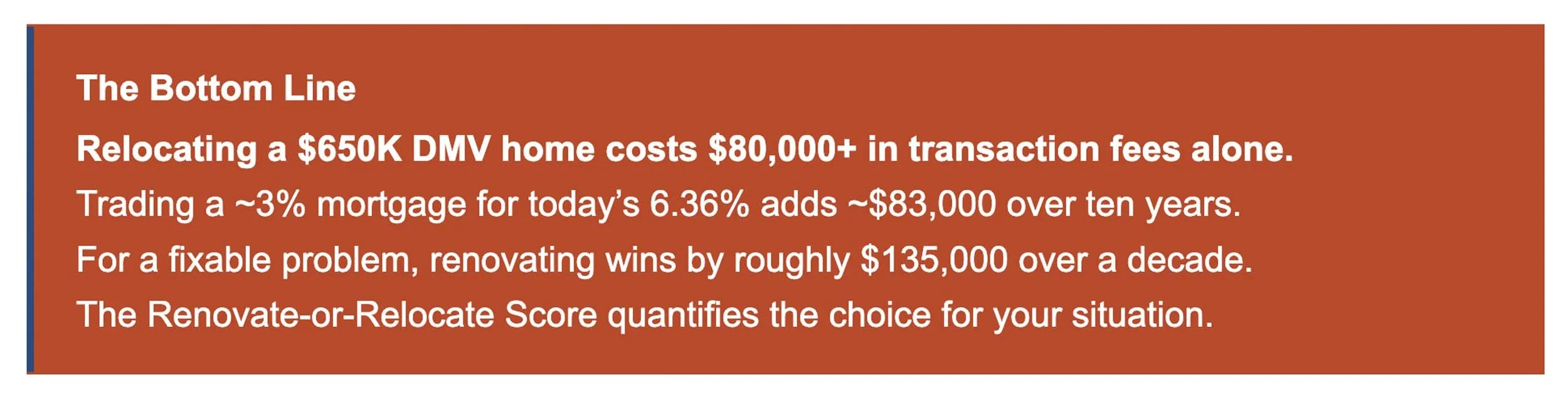

This white paper provides that analysis. Using the current 30-year mortgage rate of 6.36% as of May 2026, real transaction-cost data, permit trends across seven DMV jurisdictions, and a ten-year cost model, we quantify the true cost of each path. The conclusion is consistent and, for many homeowners, surprising: for the typical DMV household addressing a fixable functional gap, renovating and staying is dramatically cheaper than selling and rebuying — by roughly $135,000 over a ten-year horizon.

The reason is not the visible cost of renovation versus the visible cost of moving. It is the hidden costs of relocating: the $80,000-plus in transaction fees required simply to change addresses, and — larger still — the mortgage rate reset, the penalty a homeowner pays for trading a pandemic-era loan near 3% for a new loan above 6%. Together these costs form a moat around the home a family already owns.

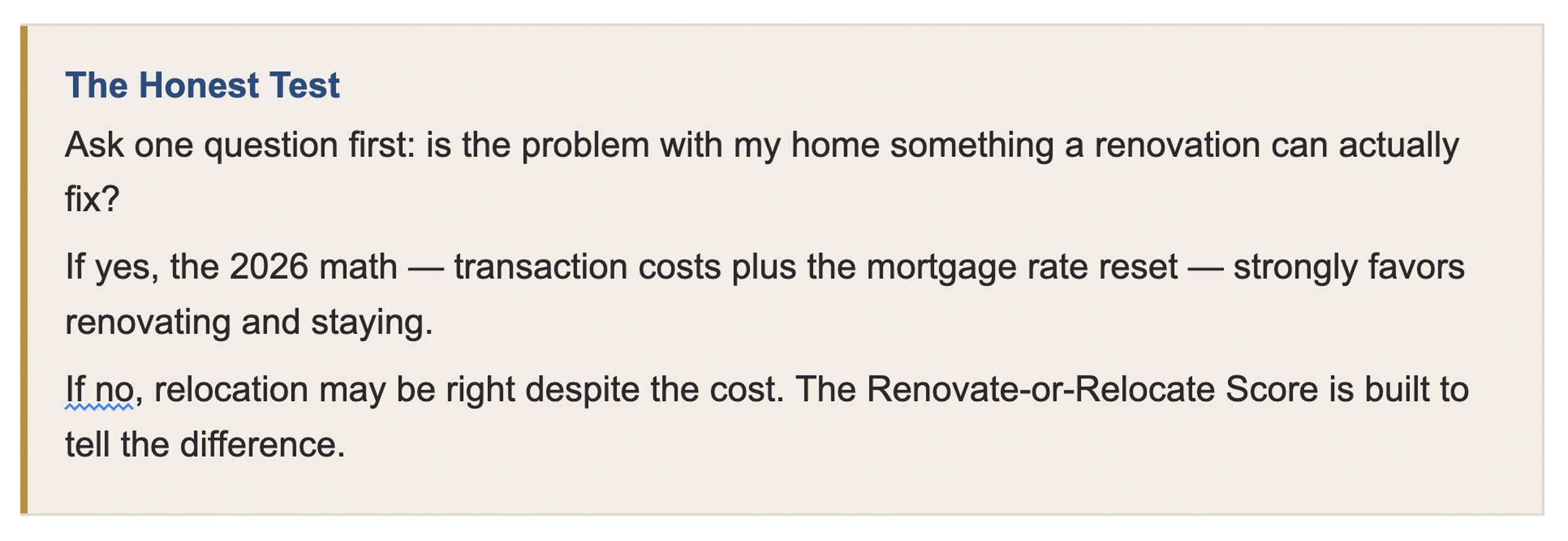

This is not an argument that no one should ever move. Relocation is the right answer when a home’s problem cannot be renovated away — a location, a commute, a school district, a lot. The final section of this report introduces the Renovate-or-Relocate Score, a 0–100 framework any DMV homeowner can apply to their own situation to determine, with clarity, which path the numbers favor.

The True Cost of Relocating

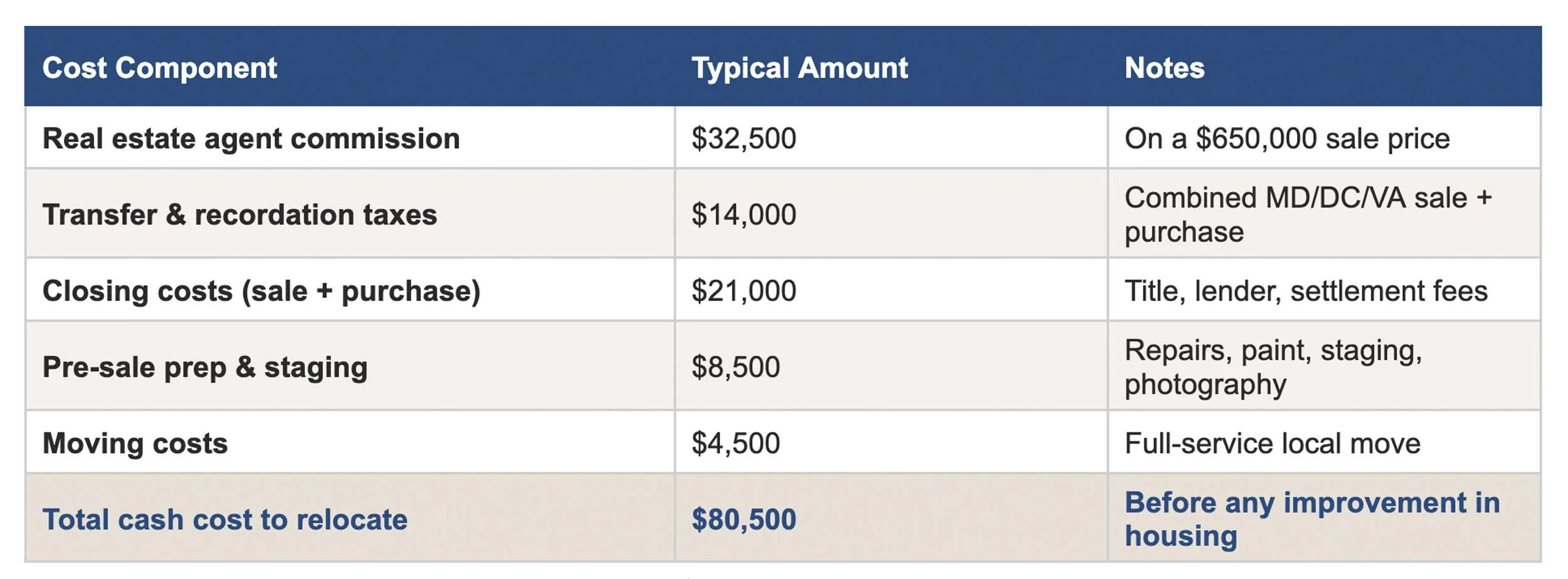

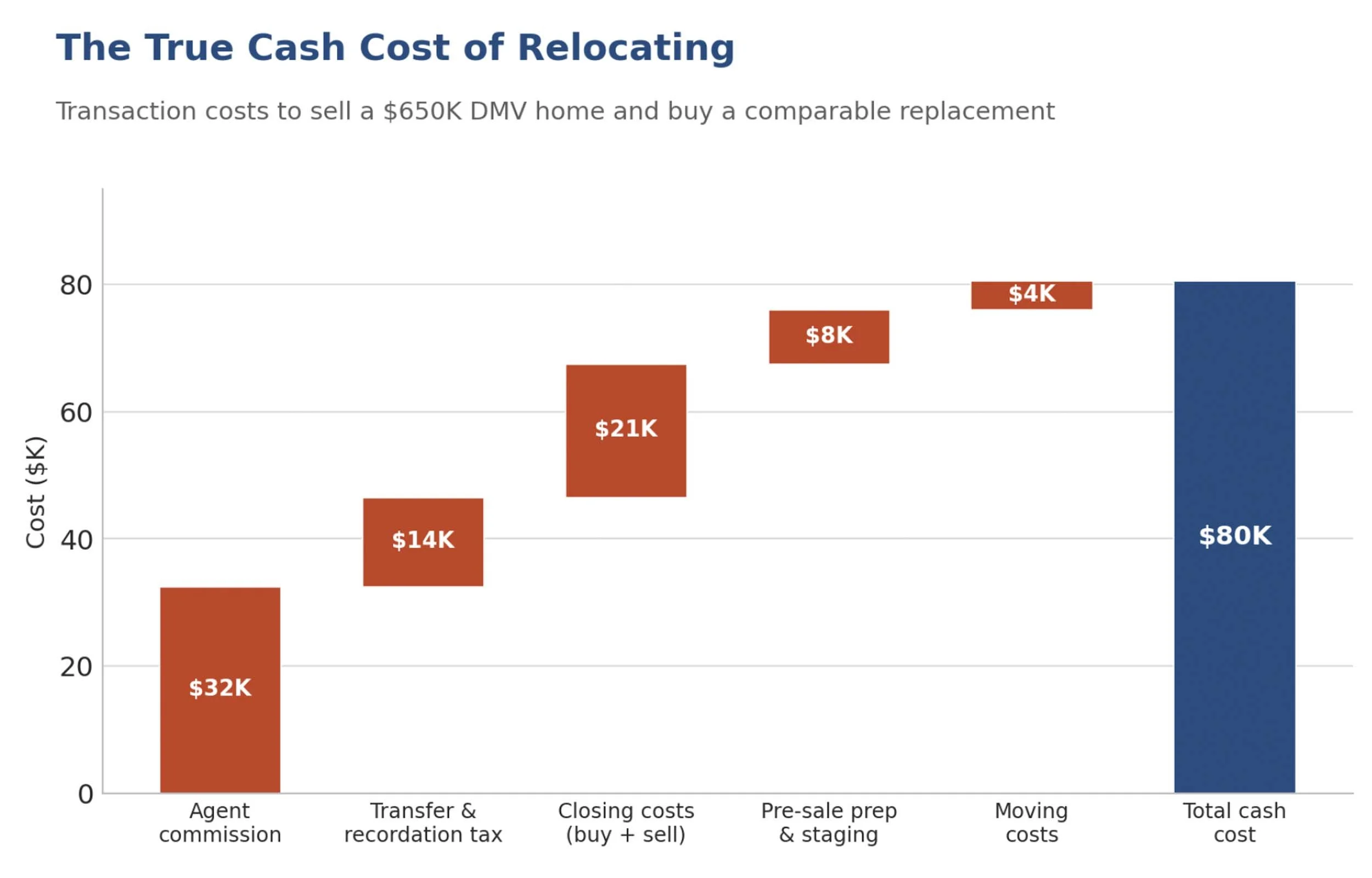

Most homeowners dramatically underestimate the full cost of selling one home and buying another. The visible costs — the agent commission, the closing fee — are only part of the picture. When every line item is accounted for, the cash cost of relocating within the DMV is substantial before the family has improved its housing situation by a single square foot.

Transaction cost of relocating, modeled on a $650,000 DMV home. Source: MD/VA/DC transfer-tax schedules; Bright MLS; RemodelTrends.com.

The cash cost of selling a $650K DMV home and buying a comparable replacement.

The figure of $80,500 is the price of admission — the amount a homeowner spends simply to convert one home into another of equal value. It buys no additional space, no updated kitchen, no finished basement. And critically, it is real cash, paid at settlement, not financed over time. For a homeowner whose actual goal is more space or an updated home, that $80,500 represents pure friction — money that a renovation budget would instead convert directly into improvements the family uses and an asset that recovers most of its cost at resale.

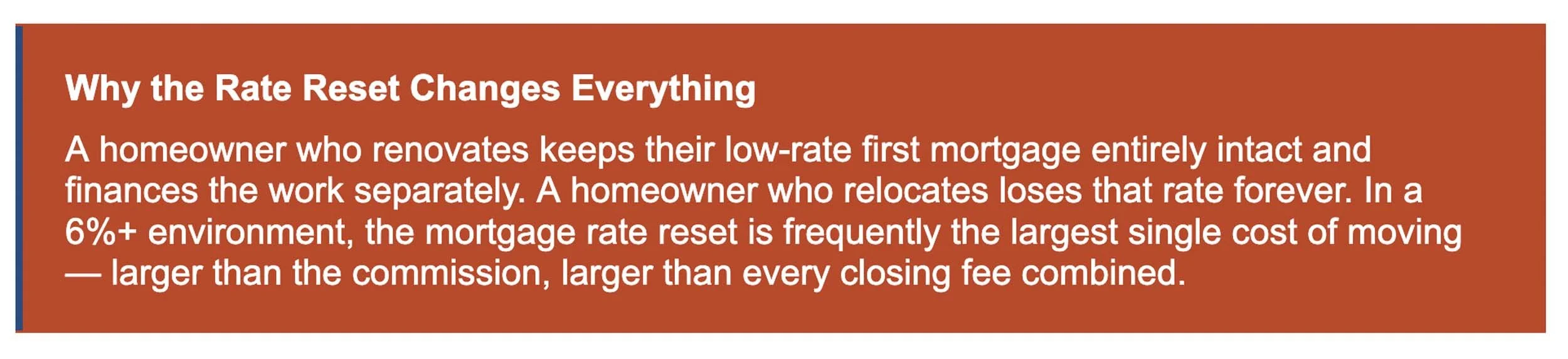

The Hidden Cost: The Mortgage Rate Reset

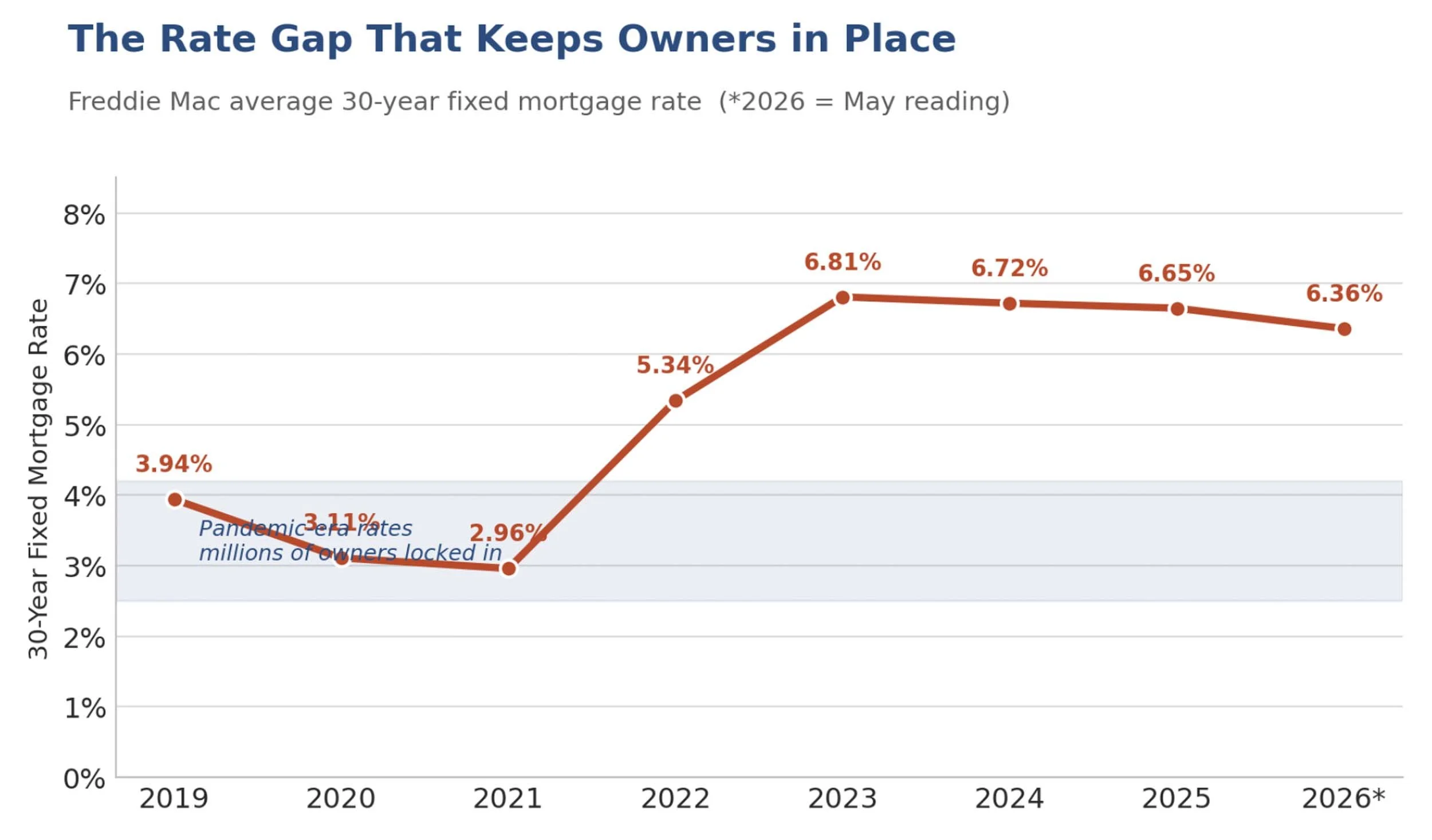

The $80,500 in transaction costs is the visible barrier to relocating. The larger barrier is invisible on any settlement statement, and it is the single most important financial fact of the 2026 housing market: the mortgage rate reset.

Freddie Mac average 30-year fixed mortgage rate, 2019–2026.

Between 2020 and 2022, mortgage rates fell to the lowest levels in American history — bottoming near 2.96% in 2021. A large share of DMV homeowners either bought or refinanced during that window and now hold mortgages at rates between roughly 2.75% and 4%. Today, the 30-year fixed rate stands at 6.36%. A homeowner who sells and buys a new home does not merely pay transaction costs — they surrender their low-rate mortgage and take on a new one at more than double the interest rate.

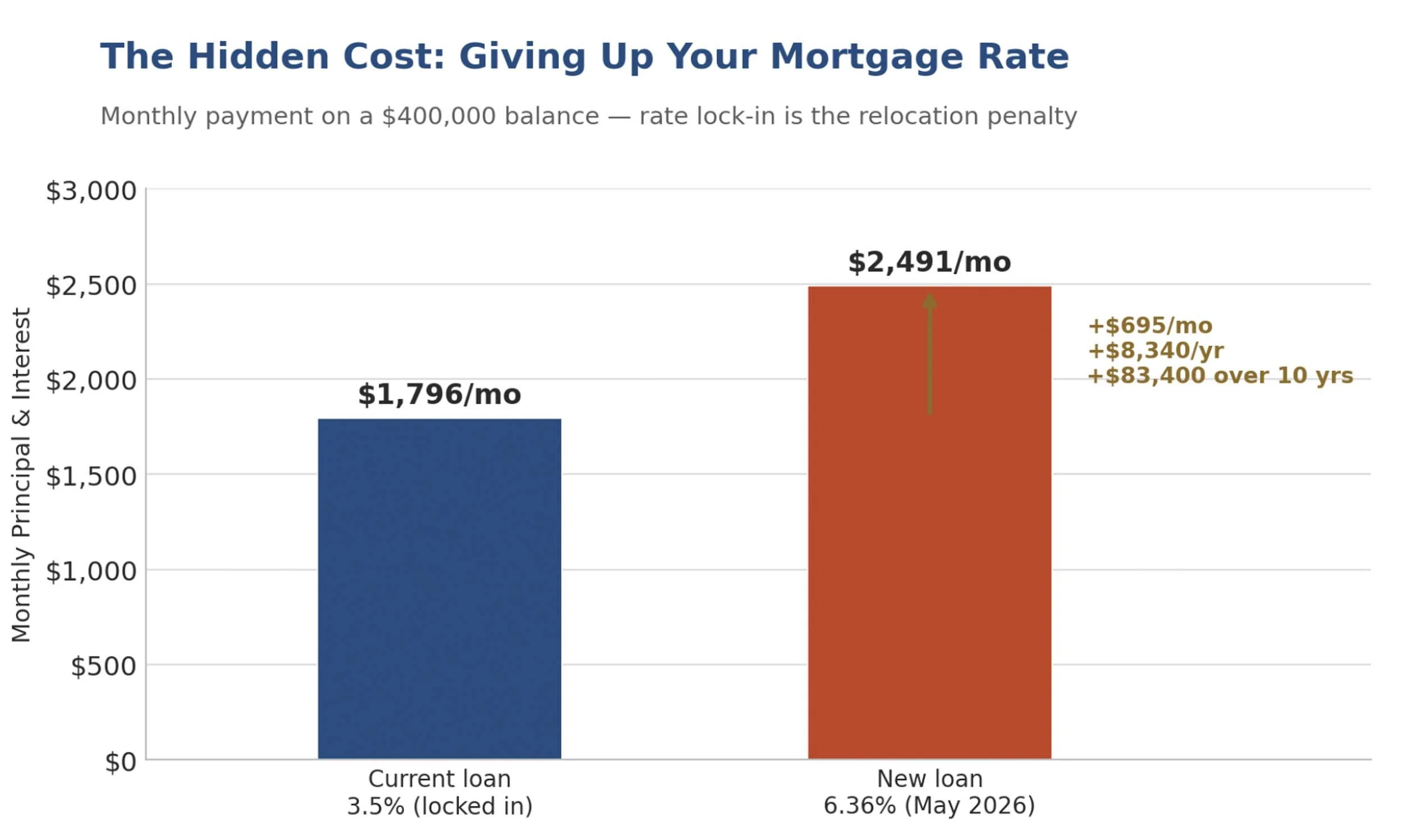

Monthly payment on a $400,000 loan balance: a locked-in 3.5% rate vs. today’s 6.36%.

The arithmetic is stark. On a $400,000 loan balance, a 3.5% rate produces a monthly principal-and-interest payment of about $1,796. The same balance at 6.36% costs about $2,491 per month. That difference — $695 every month, $8,340 every year, more than $83,000 over a ten-year period — is the true price of giving up a pandemic-era mortgage. It is why economists describe today’s market as “locked in”: millions of homeowners are financially anchored to their current homes not by sentiment, but by an interest-rate gap that makes moving extraordinarily expensive.

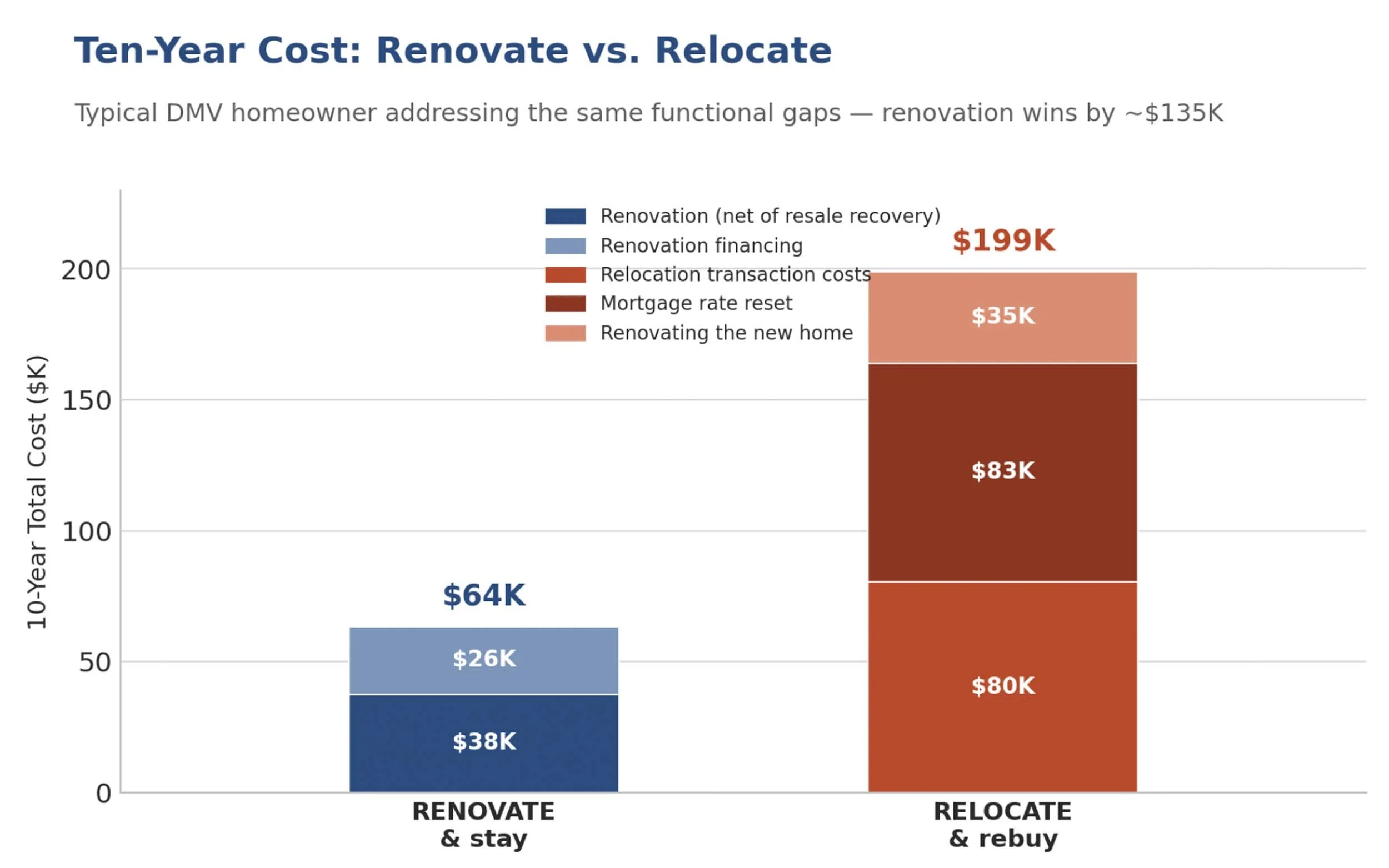

Renovate vs. Relocate: The Ten-Year Comparison

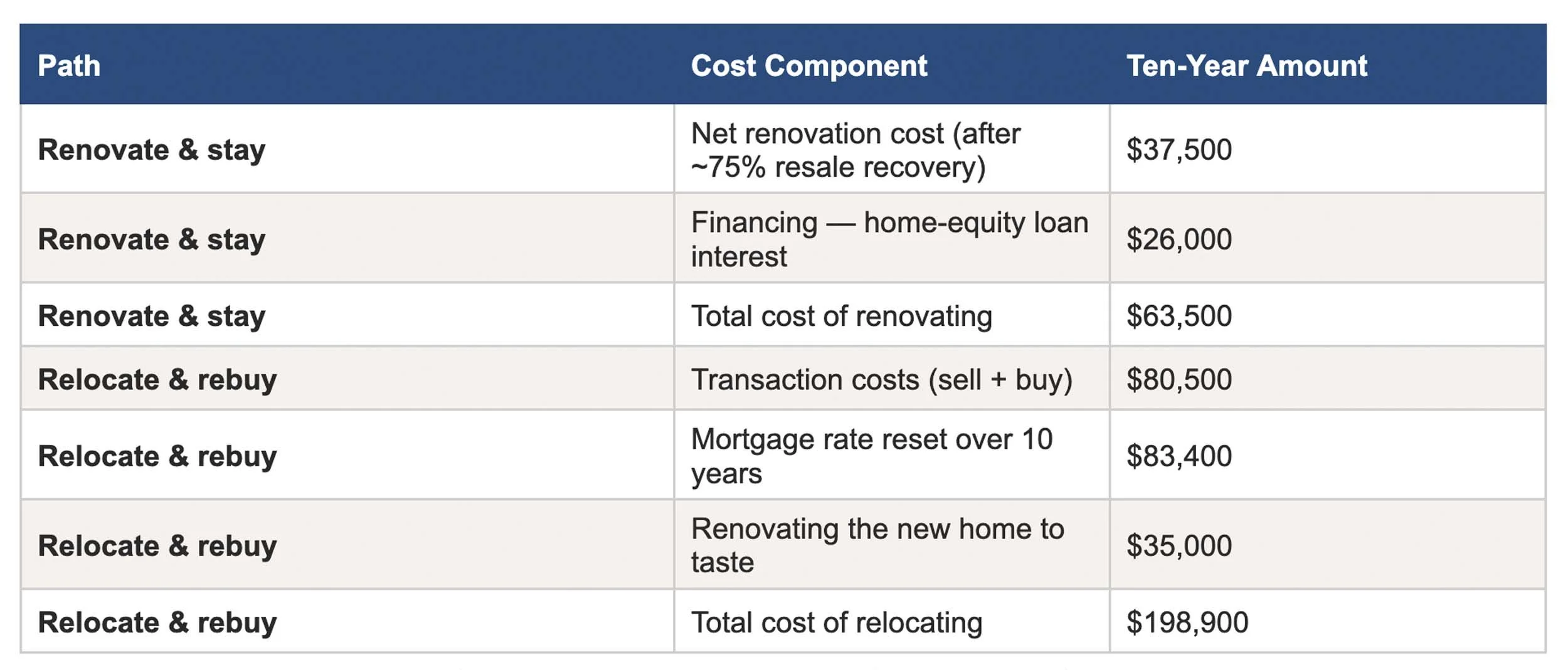

To compare the two paths fairly, we model a representative DMV household with a specific, solvable problem: the home is too small or too dated for the family’s needs, and the fix would cost about $150,000 as a renovation. The household can either renovate to solve the problem, or relocate to a larger, updated home of comparable market tier. The table and figure below total the cost of each path over a ten-year horizon.

Ten-year cost comparison for a household solving the same functional gap. Source: RemodelTrends.com economic model.

Ten-year total cost: renovating and staying vs. relocating and rebuying.

The gap is decisive. Renovating and staying costs the modeled household about $63,500 over ten years; relocating and rebuying costs about $198,900. The renovation path wins by roughly $135,000. Two facts drive the result. First, a renovation is not a pure expense — a well-chosen project recovers an estimated 75% of its cost at eventual resale, so the true net cost is a fraction of the sticker price. Second, the relocation path carries the full $80,500 in transaction costs and the full $83,400 rate-reset penalty — and the family that moves to a new home very often renovates that home anyway, adding cost rather than avoiding it.

The lesson is not that renovation is free. It is that renovation converts spending into a usable improvement and a recoverable asset, while the largest costs of relocation — transaction friction and the rate reset — buy the family nothing at all.

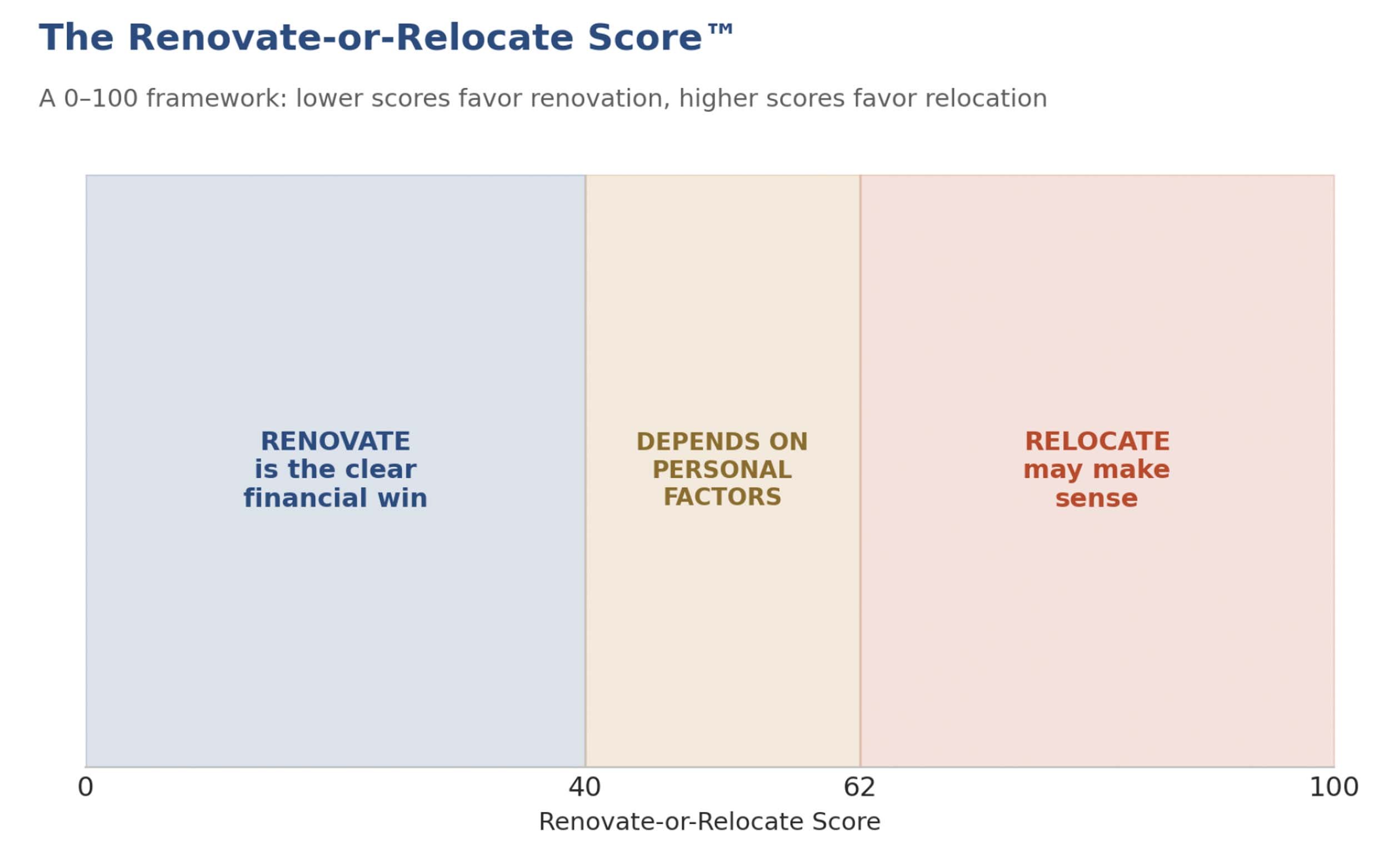

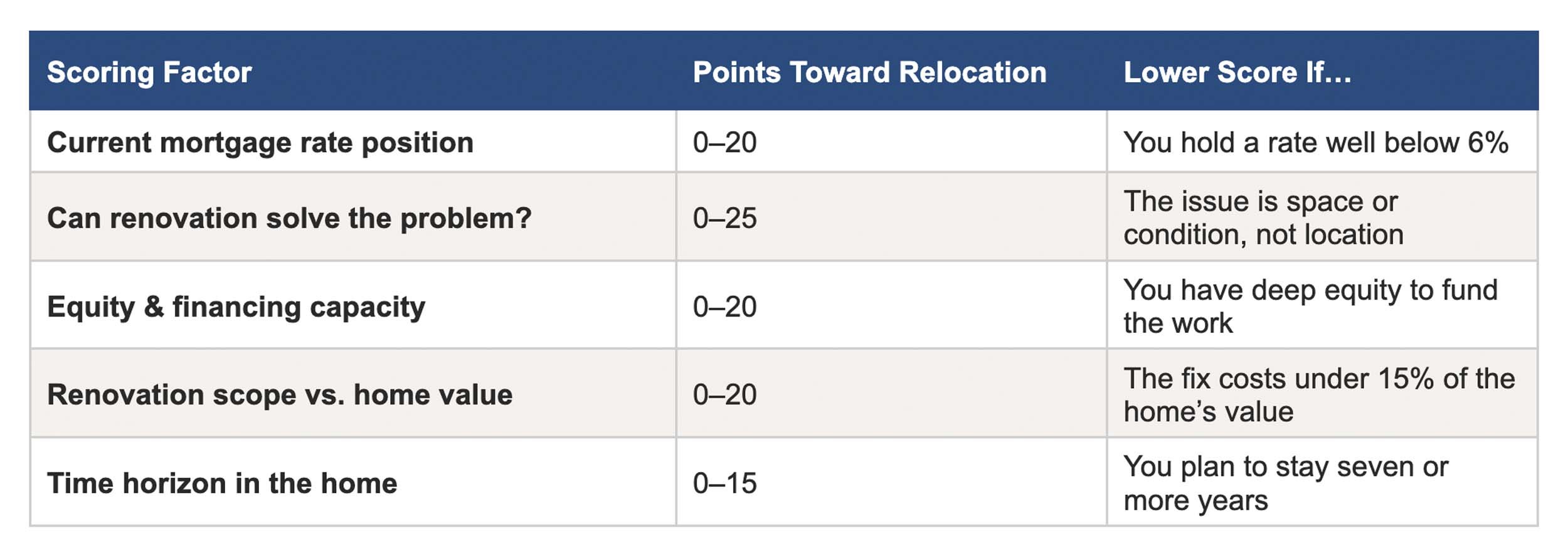

The Renovate-or-Relocate Score

The ten-year model assumes the household’s problem is one that renovation can actually solve. That assumption does not always hold — and when it fails, relocation can be the right choice regardless of cost. The Renovate-or-Relocate Score is a simple framework for testing it. The homeowner scores their situation across five factors; the factors sum to a 0–100 total, where lower scores favor renovation and higher scores favor relocation.

The Renovate-or-Relocate Score and its decision zones.

The five factors of the Renovate-or-Relocate Score. Maximum total: 100 points.

Reading Your Score

A total below 40 places a homeowner firmly in the “Renovate” zone: the problem is fixable, the mortgage rate is worth protecting, and the equity exists to fund the work — renovation is the clear financial winner. A score between 40 and 62 falls in the “Depends” zone, where personal factors — family timing, risk tolerance, how much a particular neighborhood matters — legitimately tip the decision either way. A score above 62 indicates the “Relocate” zone: the home’s core problem is one renovation cannot reach, and a move is justified despite its cost.

The Score’s value is that it separates the two questions homeowners usually tangle together: “is moving worth the cost?” and “can my problem be renovated away?” Most homeowners who run the framework honestly discover that their problem is, in fact, fixable — and that the rate reset and transaction costs make renovation the rational choice.

When Relocation Still Makes Sense

This report is an economic analysis, not a blanket recommendation. There are clear, legitimate situations in which relocation is the right decision even with the rate reset and transaction costs fully counted. They share one characteristic: the home’s problem is something renovation cannot change.

LOCATION AND COMMUTE — renovation can expand a house, finish a basement, or modernize a kitchen — it cannot move the home closer to work, family, or a preferred school district.

LOT AND STRUCTURAL LIMITS — a lot that is genuinely too small for the family’s needs, or a home whose structure cannot accommodate the required addition, sets a hard ceiling renovation cannot raise.

LIFE-STAGE CHANGE — for a household downsizing in retirement, the goal is less house, not an improved one — relocation is the natural path.

OVER-IMPROVEMENT RISK — when a renovation would cost more than roughly 35–40% of the home’s value, the project risks over-improving for the neighborhood, and relocation deserves serious weight.

SHORT TIME HORIZON — a household that knows it will move within two to three years for reasons unrelated to the house gains little from a major renovation it will not enjoy for long.

What This Means for DMV Homeowners

Run the Numbers Before the Emotions

The Renovate-or-Relocate decision is genuinely emotional, and emotion tends to favor the fresh start of a move. The discipline this report recommends is simple: quantify both paths before deciding. Total the transaction costs, calculate the rate-reset penalty against your actual current mortgage rate, and compare them honestly against a renovation estimate. The numbers are frequently more lopsided than homeowners expect.

Protect the Asset You Already Hold

A low-rate mortgage secured in 2020 or 2021 is, in today’s market, a valuable financial asset in its own right. Renovating allows a homeowner to improve their housing while keeping that asset fully intact, financing the work through a separate home-equity facility. Relocating forfeits it permanently. In a 6%+ rate environment, that single fact reshapes the entire decision.

Plan the Renovation Like an Investment

If the analysis points to renovating — as it does for most homeowners with a fixable problem — approach the project strategically. Prioritize the work that solves the actual functional gap, choose durable midrange finishes that appeal to future buyers, and sequence the projects so the spending is deliberate rather than reactive. Done well, a renovation does not just resolve the problem that prompted the renovate-or-relocate question. It produces a home the family is glad to keep.

Methodology

Mortgage rates in this report are drawn from the Freddie Mac Primary Mortgage Market Survey; the 6.36% figure reflects the survey reading for mid-May 2026. The rate-reset calculation compares the monthly principal-and-interest payment on a $400,000 loan balance at a representative locked-in rate of 3.5% against the same balance at 6.36%, using standard amortization, over a ten-year holding period.

Transaction costs are modeled on a $650,000 DMV home and reflect prevailing real estate commissions, the combined transfer and recordation tax schedules of Maryland, Virginia, and the District of Columbia, and typical settlement, preparation, and moving costs as observed in Bright MLS data. The ten-year comparison and the Renovate-or-Relocate Score are proprietary RemodelTrends.com frameworks intended as decision-support tools; individual outcomes will vary with a homeowner’s mortgage rate, equity, and project scope.

About Four Seasons Home Improvement

Four Seasons Home Improvement is a full-service home improvement contractor serving Washington, D.C., Maryland and Northern Virginia since 1976, with a focus on roofing, siding, windows, kitchens, bathrooms, and exterior renovations.

We combine decades of hands-on construction experience with data-driven insights from RemodelTrends.com, a leading proprietary analytics platform that analyzes building permit data across the Mid-Atlantic region.

This report concludes our 2026 DMV Permit-Data White Paper Series. It builds on our companion reports examining the regional renovation cycle, the timing of major-system replacement, and remodeling ROI for older homes — together, a complete framework for the decisions DMV homeowners face in the decade ahead.

If you’re ready to start your home improvement project with a proven team that has served the DMV since 1976, get in touch for a free estimate today.